Genova: This Japanese Microcap Just Acquired a Bankrupt Dental SaaS

Founder-led, capital-light, misunderstood margin dip, trading at 9× earnings with SaaS-like unit economics and a 40% IRR setup

Genova, Inc., listed on the Tokyo Stock Exchange under the ticker symbol 9341, operates in Japan's burgeoning healthcare technology sector. This article aims to delve into the intricacies of Genova's business model, its position within the Japanese healthcare landscape, its financial performance, and the potential opportunities and risks associated with investing in the company. As the healthcare industry globally embraces digital transformation, understanding the dynamics of companies like Genova becomes increasingly pertinent for investors seeking exposure to this evolving market.

Company History

Genova, Inc. was founded in July 2005 in Tokyo as a web content development firm focused on medical institutions. It quickly launched its proprietary CMS for clinics, laying the groundwork for its healthcare technology focus. Between 2009 and 2013, Genova expanded regionally, opening offices in Osaka, Fukuoka, Okinawa, and internationally in Dalian, China. The company diversified its offerings with services like PLIMO, SUPER PLIMO, and Genom, catering to mobile and responsive CMS needs. By 2015, Genova restructured to specialize in healthcare sales, introducing the NOMOCa suite for clinic automation, including self-check-in and payment systems. Subsequent years saw the launch of CLINIC BOT, a chatbot system, and the establishment of subsidiaries like GENOVA Marketing and Genova Design. In 2022, Genova was listed on the Tokyo Stock Exchange Growth Market (TSE: 9341).

What Does Genova Do? A Deep Dive into Their Business

Our company is a healthcare tech firm with a mission of “Creating a Healthy Society by Connecting People and Medical Care.” We are committed to addressing social issues in Japan such as the shortage of medical personnel due to a declining birthrate and aging population, and the growing burden of national healthcare costs. We are committed to resolving patients’ and users’ concerns and dissatisfaction regarding healthcare and wellness through our services, creating a healthy society by connecting people and medical care.

Genova operates primarily in two interconnected business segments: the Medical Platform business (Healthcare Infrastructure) and the Smart Clinic business (Clinic Automation). The company's core focus lies in providing support for web marketing and enhancing the operational efficiency of clinics, which are defined as healthcare facilities with 19 beds or fewer, across Japan. This specific focus indicates a strategic niche targeting a significant segment within the Japanese healthcare system. Unlike larger hospitals that may have already invested heavily in digital infrastructure, smaller clinics represent a potentially underserved market with distinct needs regarding patient outreach and daily operations.

The Medical Platform business, centered around their "Medical DOC" platform, is a comprehensive resource for medical institutions and the general public. This platform functions as a distribution channel for various types of content, including articles authored by medical institutions, narratives of patient experiences, informative treatment videos, and a broad range of medical-related articles. Furthermore, Medical DOC incorporates an extensive database containing information on medical institutions throughout Japan, allowing users to easily search for facilities based on geographical location or medical specialty. The platform offers medical institutions a valuable opportunity to enhance their visibility and attract new patients by showcasing their unique services and treatment approaches. The primary revenue stream for this segment is generated through fees paid by clinics for creating these introductory articles, with revenue being recognized as a lump sum upon the initial production of the content. In the fiscal year ending March 2024, the average contract unit price for these articles stood at JPY1.370 million, marking a 5.7% year-over-year increase, while the total contract volume for the year reached 3,804, representing a substantial 24.2% increase compared to the previous year. This growth in both the average price and the number of articles suggests a strong and increasing demand from clinics for the marketing services provided by Genova's platform.

The Smart Clinic business addresses the operational challenges faced by medical institutions through a suite of technology-driven solutions. This segment includes an online medical treatment and consultation service branded as "Smart Clinic," enabling patients to receive medical attention from the convenience of their homes or workplaces, eliminating the need to visit a hospital. Additionally, Genova offers a range of hardware and software products under the "NOMOCa" brand, including the NOMOCa-Stand, a smart and user-friendly automatic payment and reception machine; the NOMOCa-Regi, a self-service payment terminal specifically designed for clinics; and CLINIC BOT, an AI-powered chatbot system leveraging the widely used LINE messaging application for customer relationship management. The NOMOCa series of products is specifically designed to alleviate the administrative burden on medical staff within clinics. The revenue model for the Smart Clinic business is based on the direct sale of both the hardware equipment and the associated software licenses. In the fiscal year ending March 2024, hardware sales constituted 64.3% of the segment's total revenue, with software contributing the remaining 35.7%. The average unit prices during this period were JPY2.316 million for hardware and JPY812,000 for software, with a contract volume of 464 units for hardware and 1,084 contracts for software. The CLINIC BOT service allows patients to easily make reservations or inquiries through the popular LINE social media application, further streamlining clinic operations and enhancing patient convenience. The Smart Clinic business thus provides a more tangible and diversified revenue stream for Genova, extending beyond the marketing focus of the Medical Platform segment.

Genova's primary target market consists of approximately 173,000 medical and dental clinics across Japan. This excludes larger healthcare facilities such as universities and general hospitals, which are presumed to have already made significant progress in adopting digital technologies. As of the fiscal year ending March 2024, Genova had accumulated a total of 14,000 customers, representing a penetration of just 8.1% within its estimated potential customer base. This relatively low penetration rate suggests a substantial runway for future growth within their existing target market. To capitalize on this opportunity, Genova has outlined plans to expand its sales operations, aiming to have 10 sales offices in place by the fiscal year ending March 2025. This strategic expansion of their nationwide sales network is intended to improve their reach and facilitate the acquisition of new customers.

Decoding the Economics of Genova's Business

Genova's revenue generation is derived from distinct mechanisms within its two primary business segments. The Medical Platform business operates on a model that resembles a subscription service, with clinics paying fees for the creation of marketing articles that are then hosted on the Medical DOC platform. This generates a relatively stable and recurring revenue stream as clinics continuously seek to attract new patients. In contrast, the Smart Clinic business employs a more diversified approach, generating revenue through a combination of upfront sales from the hardware products, such as the NOMOCa-Stand and NOMOCa-Regi machines, and recurring fees associated with the software and services, most notably the CLINIC BOT system. This blend of revenue models could offer a degree of financial stability, balancing immediate income from hardware sales with the more predictable long-term revenue associated with software subscriptions and service agreements.

Analyzing Genova's cost structure reveals different dynamics at play within each segment. The Medical Platform business likely incurs its primary costs through personnel involved in content creation, platform development, and ongoing maintenance. These costs may exhibit a degree of fixedness, particularly concerning the underlying infrastructure of the platform. The Smart Clinic business, however, includes the significant cost of purchasing the hardware equipment that is then sold to clinics, directly impacting the gross profit margin for this segment. In the fiscal year ending March 2024, the overall gross profit margin for the Smart Clinic business was reported at 48.4%, with a notable difference between the NOMOCa products (31.2%) and the CLINIC BOT service (79.4%). This disparity highlights the higher profitability associated with the software component of the Smart Clinic business. Overall, the gross profit margin for the Medical Platform business is observed to be higher in comparison to the Smart Clinic business, primarily due to the absence of substantial direct product costs. This suggests that the Medical Platform segment is inherently more profitable on a per-unit basis. However, the Smart Clinic segment, with its potential for recurring software revenue, could contribute significantly to long-term profitability and customer stickiness. Understanding the specific drivers behind these differing margin profiles is essential for evaluating Genova's future earnings potential.

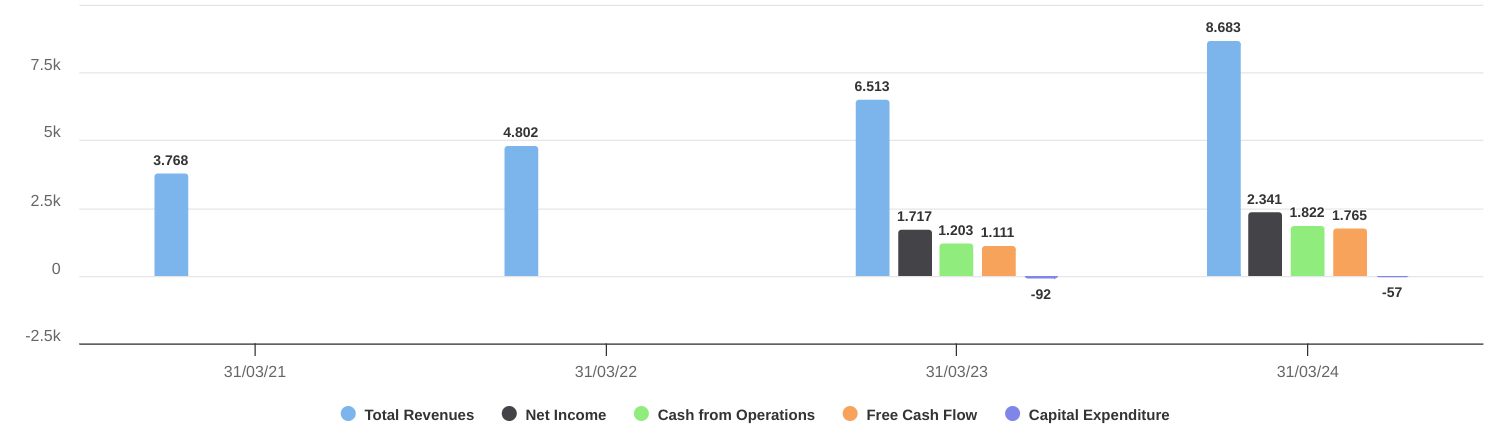

Genova has demonstrated a strong track record of financial growth in recent periods. In the calendar year 2023, the company reported revenue of JPY8.68 billion, marking a substantial 33.32% increase compared to the JPY6.51 billion recorded in the previous year. Earnings for the same period reached JPY1.73 billion, representing an even more impressive growth of 36.98% year-over-year. Looking at the trailing twelve months as of April 2025, Genova's revenue reached JPY10.19 billion, with a net income of JPY1.87 billion.

The earnings per share (EPS) for the trailing twelve months have been reported in the range of JPY103.89 to JPY107.78. This consistent and significant growth in both revenue and earnings suggests that Genova's business model is effectively capturing the opportunities within the Japanese healthcare technology market.

Regarding the nature of Genova's costs, it is likely that the company experiences a blend of both fixed and variable expenditures. Platform development and ongoing maintenance for the Medical DOC and Smart Clinic services would likely represent a more fixed cost base. Conversely, expenses related to content creation for the Medical Platform and sales and marketing efforts would likely fluctuate more directly with the level of business activity, making them more variable. Notably, the cost of the hardware equipment sold within the Smart Clinic segment represents a significant variable cost that is directly tied to sales volume. A crucial aspect for investors to consider is the scalability of Genova's cost structure. The ability to increase revenues without a proportional increase in operating costs would be a strong indicator of the company's operational efficiency and potential for enhanced profitability in the future.

Investment Thesis: Strengths and Opportunities

The long-term outlook for Genova is closely tied to the ongoing digitization of the healthcare sector in Japan. While Japan's healthcare system is internationally recognized for its quality and accessibility, the adoption of digital technologies within the primary care sector has lagged behind other developed nations. For instance, a 2023 survey indicated that the adoption rate of electronic medical records (EMRs) in Japanese primary care was only 42% in 2021, significantly lower than the OECD average of 93%. This gap signifies a substantial opportunity for companies like Genova that offer digital solutions tailored to the needs of clinics. The broader Japanese healthcare IT market is projected to experience considerable growth in the coming years, with revenue forecasts reaching USD 33.76 billion by 2030, representing a compound annual growth rate of 14.4% from 2024. This favorable market trend provides a strong tailwind for Genova's business operations, as the increasing adoption of digital solutions by clinics is likely to drive demand for their services and products.

Genova appears to have carved out a strategic position within this market by focusing specifically on smaller clinics with 19 beds or fewer. This niche focus may offer a less competitive landscape compared to the market for solutions targeting large hospitals, which often have more complex and established IT infrastructures. Furthermore, Genova's strength lies in its integrated suite of solutions that address both the web marketing and operational efficiency needs of clinics. By offering a comprehensive package, Genova can potentially build stronger and more valuable relationships with its clients. The inclusion of CLINIC BOT, which leverages the widely popular LINE messaging app, could also provide a significant competitive advantage by offering a familiar and user-friendly interface for both clinic staff and patients. This ease of use can be a crucial factor in driving adoption among smaller medical practices.

Japan's rapidly aging society presents another significant long-term driver for Genova's growth. The increasing proportion of elderly individuals is expected to lead to a greater demand for healthcare services, particularly at the primary care level, which is the focus of Genova's client base. Moreover, the Japanese government has been actively promoting regional healthcare initiatives and aiming to strengthen the role of primary care physicians. These policy directions suggest an expanding role for clinics in the overall healthcare ecosystem, which could further benefit Genova as these clinics seek to enhance their operations and patient outreach through technology.

Why the Opportunity Exists Now

The market is reacting to margin compression—and that’s exactly where the opportunity lies.

In FY03/25, Genova’s gross margin declined to 72.3%, a drop of 3.6 percentage points quarter-over-quarter. This was largely due to a shift in revenue mix, as the company booked a higher share of lower-margin service contracts in its Medical Platform business and invested in more costly content types, such as treatment videos. At the same time, the Smart Clinic segment—Genova’s second growth engine—experienced a slowdown in hardware orders, while bearing the upfront costs of launching new services like NOMOCa AI chat and NOMOCa AI call.

Operating margins were hit even harder, falling from 24.1% in Q2 to 16.6% in Q3, due to a 26.4% YoY spike in SG&A. These rising costs came from several deliberate investments: expanding the salesforce, opening new regional offices, and increased spending on product development and marketing. In fact, Smart Clinic’s operating margin dropped to just 10.7%, as management prioritized long-term capability building over short-term profitability.

For many investors, this kind of temporary margin erosion is a red flag. But for others, it signals timing. Genova is investing ahead of the curve—expanding distribution, onboarding new services, and setting up the infrastructure to support what it expects to be significantly higher volume in 2026 and beyond. Management has already guided for a recovery to ~25% operating margins by year-end, reinforcing the idea that this compression is both cyclical and strategic.

In short, Genova’s stock is weak right now because its margins are. But the margin pressure isn’t due to deterioration—it’s due to deliberate reinvestment. That makes this a classic setup: high-growth fundamentals, misunderstood near-term financials, and a valuation that doesn’t reflect what the company might look like 12–18 months from now. Investors who can see through the noise may be getting a compounder on sale.

Navigating the Risks: Potential Pitfalls

Despite the promising outlook, potential investors should be mindful of the risks associated with Genova. The healthcare IT market in Japan is an evolving landscape that is likely to attract more competitors over time, including potentially larger and more established technology companies. While Genova currently focuses on a specific niche of smaller clinics, the success of this segment could attract direct competition. Furthermore, the regulatory environment surrounding healthcare and technology adoption in Japan could undergo changes that might impact Genova's business operations and growth trajectory. The rapid pace of technological advancements in areas like artificial intelligence also necessitates continuous innovation and adaptation from Genova to maintain its competitive edge. Finally, while the potential market size for Genova's services is substantial, the company's ability to effectively acquire and retain clinics as paying customers will be critical for achieving sustained growth and profitability.

In addition, Genova faces several internal and structural challenges that investors should consider. High employee turnover, particularly within the salesforce, threatens to erode client relationships and create friction in the company’s ability to convert and upsell clinics—especially in a relationship-driven industry like healthcare. Rising recruitment costs only add to this burden. The company is also heavily reliant on dental clinics, which make up about 60% of its client base. With a shrinking pipeline of younger dentists and a projected long-term decline in dental clinic numbers, this concentration risk could limit future growth. Moreover, Genova’s main hardware offering—automated payment machines—is not proprietary and sourced from third-party manufacturers, exposing it to price competition and product commoditization. Larger hardware players like Hitachi and NEC are already entering the clinic segment, increasing the pressure on Genova to defend its margins and retain differentiation.

Management and Ownership: Assessing the Human Factor

The leadership of Genova, Inc. is headed by CEO Tomoki Hirase, with Akinao Ueda and Koji Takeda serving as fellow board members. The board also includes external members Yuki Sagehashi, Motoaki Fukui, Takaaki Suzuki, and Ayako Miwa, bringing diverse perspectives and expertise. The company's auditing functions are overseen by external auditors Tsuyoshi Sasaki and Yasuo Goto, who serve on a full-time basis.

Hirase was born in 1978 and started his career working at a printing factory before joining Telewave, a telecom startup, in 1997. He rose quickly to become a director within two years and later served as managing director of Telewave Links, playing a role in its IPO and gaining early exposure to capital markets. In 2005, he founded Genova, originally a web design firm for medical institutions. As the internet shifted toward user-generated content and demand from clinics surged, he pivoted Genova into healthcare tech.

He’s been early and deliberate in how he’s scaled the business. He moved into healthcare media in 2012 and then into clinic automation in 2017. Today, Genova is powered by two high-margin engines: Medical DOC, a physician-supervised media platform with over 14 million monthly pageviews, and Smart Clinic, a fast-growing SaaS and hardware suite for streamlining clinic operations.

Hirase is by far the largest shareholder, directly owning 41% of the company. When combined with Hirase Shoten, an affiliated entity that owns another 7.5%, his stake rises to nearly 49%. That level of insider ownership creates deep alignment with outside investors.

Capital allocation has been strong. Since FY03/21, revenue has compounded at 32.1% annually, operating profit at 42.3%, and ROE at nearly 30%. Hirase ran the company for almost 17 years without paying dividends, instead reinvesting all profits into new service lines. In 2022, Genova was listed on the TSE Growth Market and then upgraded to the TSE Prime in 2024—a notable leap in governance and scale.

He’s built a scalable, asset-light media business with gross margins above 90%. This is paired with a growing automation segment in which SaaS is gaining share over lower-margin hardware. In 2025, he acquired ADI.G, a bankrupt dental devices and cloud software business with 6,001 million yen in consolidated sales—continue reading in the next section.

Capital return has also entered the picture. FY03/25 marks the company’s first dividend (JPY 30/share) and a buyback of up to 500,000 shares (2.8% of outstanding), aimed at mitigating dilution and improving efficiency. Hirase is starting to balance growth and capital return, and doing it from a position of strength.

Acquisition Analysis – Genova × ADI.G

In April 2025, Genova announced its planned acquisition of ADI.G Corporation, a Kanazawa-based firm developing dental equipment and cloud-based solutions for clinics. The deal is expected to close for ¥825 million in cash, pending due diligence.

ADI.G brings a 50-year track record in dental hardware, materials, and design—complementing Genova’s growing Smart Clinic suite. The standout asset here is the cloud-based software for dental clinics, which aligns with Genova’s push toward high-margin, vertical SaaS.

At a headline EV/Sales of just 0.14×, the deal looks extremely cheap on a top-line basis. This suggests Genova is acquiring revenue and customers at fire-sale prices. However, the recurring profit margin is razor thin (0.3%), and the business is technically insolvent, with net liabilities > ¥3.8bn. This implies Genova is betting on restructuring and integration upside rather than immediate earnings accretion. The implied EV/Recurring Profit is ~43×, but given the near-breakeven status, this multiple isn’t very meaningful.

Genova may be acquiring proprietary cloud infrastructure and clinic relationships that it can monetize through its existing NOMOCa SaaS suite. There’s potential to convert ADI.G’s customer base into Smart Clinic subscribers, cross-selling NOMOCa AI and hardware. With prior success in transforming traditional clinic services into software platforms, Genova could repeat its “media → monetization” playbook here in dental tech. Revenue scale alone (¥6bn) could boost consolidated top line by ~50% over FY2024 levels.

However, ADI.G is financially distressed. Negative net assets and break-even profitability suggest high operational and debt-related risks. The success of this acquisition hinges on integration execution—turning hardware-heavy legacy sales into scalable software revenue. There's still uncertainty around what assets/liabilities Genova will assume. Final diligence disclosures could materially affect the deal’s attractiveness.

This is a classic distressed asset buyout, and Genova is paying what appears to be a fraction of replacement value for a sizable revenue base. While not immediately accretive to profits, it’s a strategic land grab in a fragmented and under-digitized vertical. Given Genova’s strong margin structure, product fit, and demonstrated go-to-market playbook in dental, the deal could prove highly accretive long-term.

Valuation: Is Genova Priced Right?

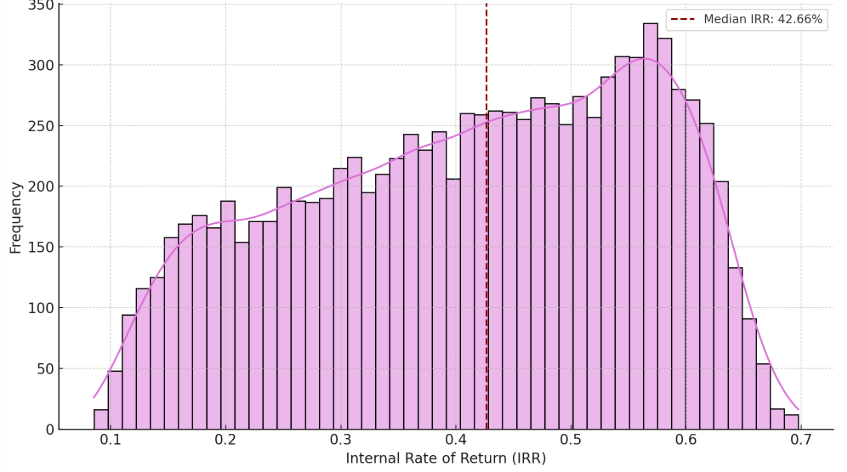

Investors in Genova could reasonably expect strong double-digit annual returns over a three-year horizon, with the Monte Carlo simulation suggesting a median IRR of 42.7%, a 90th percentile outcome of over 60%, and virtually no chance of capital loss. These projections are based on a 2024 starting EBIT of ¥2,257 million and an entry EV/EBIT multiple of 4.38—well below typical healthcare tech peers. For 2027, EBIT was modeled using a triangular distribution ranging from ¥3,700 million to ¥4,700 million, reflecting inputs from analyst forecasts, industry benchmarks, and growth implied by management's incentives. Exit valuation multiples were simulated between 3.30 and 10.45 EV/EBIT, representing the low end of distressed comparables and the upper end of high-quality SaaS peers. Even modest improvements in EBIT and a re-rating to mid-range multiples can drive substantial upside, making Genova one of the most asymmetrically positioned small-cap growth plays in Japan.

Conclusion

Genova sits at the intersection of healthcare digitization and niche vertical SaaS in Japan—a rare, capital-light player with high gross margins, solid earnings growth, and a founder who owns nearly half the business. The company has executed well so far, showing accelerating momentum across both its Medical DOC platform and Smart Clinic automation suite. Its 2025 acquisition of distressed dental cloud/software firm ADI.G marks a bold, strategic move to expand its vertical integration and grow revenue by over 50%. But this isn’t without risk—employee turnover, reliance on dental clinics, and hardware commoditization pose real execution challenges. Still, Monte Carlo simulations suggest a median IRR of over 40% with minimal downside, underscoring how attractively Genova is priced. For investors seeking asymmetric small-cap tech bets in structurally underserved markets, Genova deserves serious attention.

As always, if you enjoy deep dives like this and want to support the research, consider becoming a free subscriber. Every subscription helps keep the ideas flowing and the spreadsheets running. 🙏

Please note, this is not investment advice.

Thanks, interesting. What about the bear case - I think it is lacking. AI article generation: in that case there is no need for Genova to help doing articles. Or because its on the medical doc platform, the moat is the traffic on the platform?