Concejo AB: Berner Industrier at a Discount

Thinly traded, chairman buying, and one of the major owners of Berner Industrier, which is not reflected in its valuation — an opportunity for lumpy returns for the patient investor.

Investment Thesis

Today, investors obsess over speed, liquidity, and quarterly earnings. Concejo AB, a small, overlooked Swedish investment company, represents a different proposition: permanence, scarcity, and stewardship.

At the time of writing, Concejo carries a modest market capitalization of approximately $46.5 million. Beneath this exterior lies a collection of carefully nurtured businesses, ranging from offshore firefighting systems to cybersecurity and bioenergy, many of which are unlisted, unknown, and invisible to the investment masses.

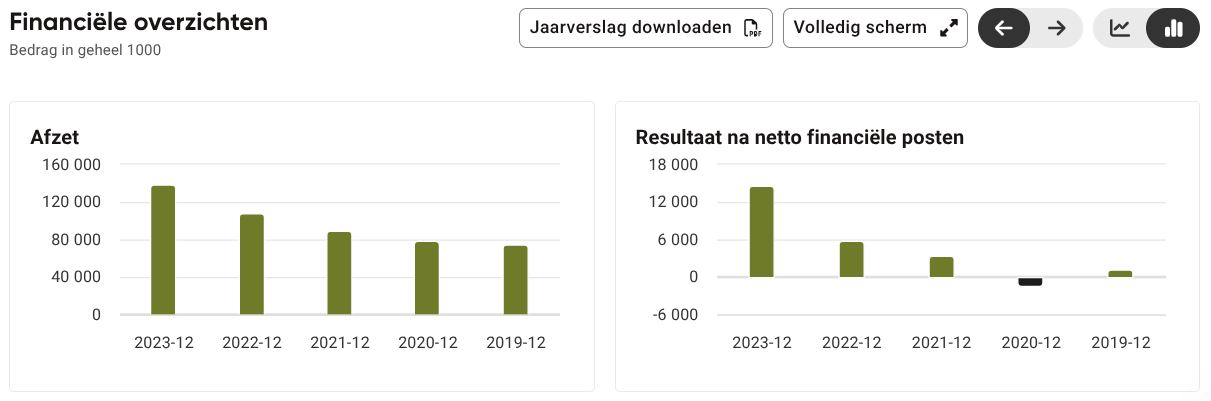

Its largest public stake, Berner Industrier, remains a textbook case in embedded optionality. Following a partial sale of 394,200 B-shares in February 2025, Concejo still holds 1,538,123 shares, valued at SEK 57.60 per share, or about SEK 88 M. Recent strength in Berner’s operating results suggests a meaningful yet unrecognized uplift in Concejo's intrinsic value - see Annex 1.

Meanwhile, insiders act not with words, but with deeds. Chairman Rickard Bergengren recently acquired 20,000 shares, investing approximately SEK 0.8 million of his wealth — a small but meaningful gesture of conviction. He acquired 199,283 shares in 2024 and 16,700 in 2023.

A Note on Origins: What Concejo Does, and Why It Matters

Before we delve into numbers and projections, we must understand the nature of what is being built.

Concejo AB, once known as Consilium, began not as a mere asset manager or financier—but as an operator, a builder of systems designed to protect life and infrastructure in unforgiving environments. Born in Sweden and headquartered in Nacka, Concejo’s heritage is fire safety: designing, manufacturing, and maintaining high-integrity safety systems for energy, offshore, and industrial applications. Its solutions range from detection and alarm systems to integrated fire suppression platforms. Its clients include those who do not get second chances: oil and gas operators, maritime fleets, and the power sector.

Over time, Concejo divested much of its navigation and non-core safety operations. A deliberate and disciplined transformation unfolded: out went the Marine & Safety division—sold to Nordic Capital in 2020 for SEK 1.5 billion—and what remained was a purer focus. The company shed parts of itself that did not serve its mission of durable value creation. The capital gains from those exits funded what Concejo has now become: a holding company that invests with stewardship, not speculation.

Today, Concejo stands on two pillars:

Concejo Industrier, anchored by Firenor International (including its 2024 acquisition of Matre Maskin), Optronics Technology, and ACAF Systems—engineers of safety systems in high-barrier, high-reliability markets.

SBF Fonder, a real asset fund manager focused on long-term residential investments in Swedish growth regions.

In 2025, the company formally wound down Concejo Ventures, consolidating non-controlling interests into a more passive portfolio. This was not retreat, but refinement.

A more detailed company overview:

Concejo Industrier:

Wholly owned operating companies, including:

Firenor (offshore fire protection; 100% acquired in 2014),

Matre Maskin (specialty engineering; acquired by Firenor in ‘24),

Optronics Technologies AS (optical sensors; 71.3% since 2018),

ACAF Systems (early-stage firefighting systems; 60% since 2017).

Associated companies (>25% ownership):

SAL Navigation (Speed Logs and Voyage Recorders; 50% acquired in 2020),

Envigas (Producer of Biocarbon; reached 25% in 2023),

Minority investments:

Berner Industrier (Nordic Industrial Group; 10,3% acquired in 2021),

Compodium (Secure Video Communications; 10,3%),

Beamwave (5G Digital Antenna Systems; 10,3%),

Others like Myra Security, Xenergic, Greenely, Urban Miners

Through SBF Fonder, Concejo also holds indirect stakes in Swedish residential property, managing approximately SEK 4.5 billion in 3,400 apartments in 20 regions.

Why This Opportunity Exists

Several factors converge to create today's opportunity:

Concejo recently ended its liquidity agreement with Carnegie Investment Bank. Without an institutional backstop, trading volumes have thinned — a condition intolerable to many, but welcome to those who cherish scarcity.

Concejo has shifted its focus from venture investments to nurturing its industrial holdings. In the words of CEO Carl Adam Rosenblad: "This means that we will no longer make new investments... Concejo Ventures has fulfilled its role as an independent business area."

Few bother to read the accounts. For those who look closely, who take the time to understand what is owned and what is built, there emerges a quiet asymmetry. The market, as usual, misjudges what it cannot count. In the fragmented noise, there is a rare information arbitrage—for the patient, for those who still believe in the value of stewardship and substance over spectacle.

Concejo trades with the dullness of a holding company, its parts weighed rather than its purpose. Yet should perception shift—from passive holder to deliberate acquirer—so too might its worth. The spark, perhaps, lies in a future separation, when form follows function and the market begins to see what patient capital already suspects.

Additional acquisitions or exits at higher multiples may provide additional upside potential, albeit lumpy. For example, in 2019, Concejo exited Consilium AB: On December 21, 2019, private equity firm Nordic Capital acquired safety/security company Consilium Marine & Safety from Concejo for 3.0B SEK. The transaction valued the business at an EV/EBITDA multiple of 12.5x, based on Consilium Marine & Safety's reported EBITDA of SEK 240 million for the twelve months ending September 2019. If Concejo sells Firenor/Matre Maskin or SAL Navigation at similar multiples, the upside can be materially higher than analysts have forecasted.

Their latest financial report notes strong growth in Optronics Technology, with net sales increasing by 113 percent, and highlights Firenor International's large order intake and expansion in the offshore wind sector. These suggest that Concejo is involved in industries with significant growth potential.

Small capitalization, limited liquidity, and obscure holdings discourage larger investors. As Deden says, "If everybody wants it, it’s not scarce."

In this environment, small and patient capital has a distinct edge.

Who Are The Owners

MCT Brattberg, the investment vehicle for the Bergengren family, owns 2,205,000 B-shares, or 18.8% of the company, and 11,1% of the voting rights. Richard Bergengren now holds 180,000 B-shares, 1.5% and 0.9% of the voting rights.

Platanen Holding AB, is the formal parent company of Concejo AB, and Platanen Holding AB’s ownership of shares in Concejo AB corresponds to 52.74 percent of all shares and 72.17 percent of the total voting value. Platanen Holding AB is controlled by the Rosenblad family.

Carl Rosenblad has been the CEO of Concejo AB since May 26, 2020, marking a tenure of approximately 4.33 years as of April 29, 2025. He has been a Board Member since 1996. During Rosenblad's tenure as CEO, the Total Shareholder Return was only ~9%, a 2% CAGR — see Annex 2 for more information.

At first glance, Concejo’s executive pay appears restrained—no bonuses, no equity, no tricks. Just fixed salary, pensions, and modest perks. Yet beneath this austerity lies a problem: management is paid the same in ruin as in reward. In 2024, the company lost over SEK 52 million, yet compensation stood untouched. Unlike peers who tether pay to results, Concejo offers no such link. This is not stewardship—it is insulation. True alignment demands consequence, not comfort.

Concejo’s capital allocation strategy focuses primarily on growing its existing businesses to meet defined targets for growth and profitability. While strategic acquisitions remain an option, current earnings are being reinvested rather than distributed as dividends.

The board intends for profits to be shared with shareholders over the long term. However, during the current growth phase, a restrained dividend policy will apply—meaning no or modest payouts. Once conditions allow, regular dividends are expected to amount to roughly 25% of profit after tax, provided that cash flows exceed the company’s investment needs and support an efficient capital structure.

What It’s Worth

"The worth of a company is measured not only by its profits but by the character of its stewards and the scarcity of its assets." — Anthony Deden

Concejo AB is not for the impatient. It builds, allocates, and quietly endures. It is a firm where much of its intrinsic value lies not in reported earnings, but in capabilities, stewardship, and the structure of its business. And yet, if one were to entertain the notion of estimating what its shares might be worth in 2027—by applying its stated financial goals and valuing each part of the business—there is, hidden beneath the surface, a potential mispricing.

What follows is not a prediction, but a model grounded in the discipline of valuation and the principles of permanence. The purpose is not to chase a target price but to understand what the business could become, if its operators remain faithful to their craft.

I. Segmenting the Enterprise: The Three Pillars of Concejo

We divide the company into three economic units:

Concejo Industrier – Comprising Firenor International (100%), Optronics Technology (71.3%), and ACAF Systems (60%)

SBF Fonder – 100% ownership of the asset management arm

Minority Investments – Stakes in SAL Navigation (49%), Envigas (25%), and small stakes in various early-stage companies

Each unit must be valued differently, by its economic characteristics— see Annex 3, 4 for more information.

In their report, Concejo mentions using IFRS 13 and the International Private Equity and Venture Capital Valuation Guidelines to value its unlisted holdings. The valuation process involves a comprehensive assessment to determine the most suitable method and reference points for each holding. While valuations from financing rounds are considered, they are not the sole method used. The techniques used include applying multiples to the companies' gross sales, net sales, and earnings. These valuations consider factors such as size, historical growth, profitability, capital costs, financial position, capital consumption, and the capital raising environment. Valuations are performed internally, and external valuations are obtained for some holdings.

II. The Targets and Their Meaning

Concejo Industrier aims to achieve an average annual growth exceeding 10 percent and a sustainable operating margin of at least 10 percent by 2027. SBF Fonder aims to increase Assets Under Management by more than 10 percent per year on average, with the management company maintaining an operating margin of at least 15 percent.

The minority investments have no explicit financial targets and must instead be treated using a range of valuation assumptions.

III. Adjusted Valuation Model – 2027

Assumptions:

2024 Revenue and EBIT for each unit based on reported numbers.

10% annual growth and target margins.

Multiples: Industrial EBIT = 12x, SBF EBIT = 15x

Ownership-adjusted values for partial holdings

The group’s industrial operations—Firenor, Optronics, and ACAF—are expected to produce roughly SEK 39 million in ownership-adjusted EBIT by 2027. Applying a conservative multiple of 12 times EBIT yields a valuation of just under SEK 470 million. Add to this SBF Fonder, a small but growing asset manager, whose expected EBIT of SEK 12.6 million, capitalized at 15 times earnings, contributes another SEK 189 million.

Among the minority holdings, two are worth noting: a 49% stake in SAL Navigation, and a 25% holding in Envigas. Taken together, these—and a smattering of unlisted micro-investments—amount to nearly SEK 200 million in conservative net present value.

Now, to what many overlook: Concejo also owns sizable stakes in three listed companies—Berner Industrier, BeammWave, and Compodium. Markets may be impatient, but prices still compound when earnings do. Applying a modest annual growth rate of 12.5% through 2027, and discounting for illiquidity, the combined value of these stakes rises to SEK 143 million.

Altogether, these core holdings bring us to a gross asset valuation of just over SEK 1 billion. But unlike Wall Street pitch decks, we must subtract what the company consumes in maintaining itself. Concejo’s group functions—central costs, in plain terms—have reliably erased SEK 30 million in EBIT each year. Moreover, it carries net debt of SEK 74 million. When both are subtracted, what remains is an enterprise worth roughly SEK 897 million.

Divide this by the 11.7 million shares outstanding, and you arrive at a 2027 intrinsic value of SEK 76.6 per share. Compared to today’s market price of SEK 39.90, the implied upside is roughly 92%. Not a bet, not a boom, but a disciplined possibility.

This is not to suggest that value will be realized. The market may continue to see a sleepy HoldCo. But time and arithmetic are allies of those who care more for solvency than for sentiment. Should perception shift—if Concejo is split, or re-rated as a serial acquirer—so too might price follow function. Until then, this remains the kind of place where capital goes not to be celebrated, but to endure.

Conclusion

Concejo is not a company for those seeking spectacle. It speaks in footnotes, not press releases. It avoids capital markets shows, preferring instead the quiet cultivation of industrial competence. Yet this silence should not be mistaken for virtue.

While the underlying businesses—Firenor, Optronics, SAL Navigation—appear to be quietly compounding in value, shareholder returns have not followed suit. The company’s transformation over the past five years, though deliberate, has yielded a mere 3.5% annual return for shareholders. For a firm claiming long-term stewardship, this is a sobering fact.

The issue is not just in what the company owns, but how it governs. Management compensation—fixed, predictable, and untouched by performance—reveals a potential disconnect. In 2024, Concejo posted a loss of over SEK 50 million. The CEO was paid the same as in any other year. It’s worth observing how this alignment will unfold, as true stewardship is demonstrated through actions, not mere proclamations. One cannot preach stewardship while practicing entitlement, but this structure holds the potential for genuine accountability.

Nevertheless, a shift is occurring—possibly influenced by the presence of the Bergengren family. The core holdings are improving. Optronics is growing rapidly. Firenor is expanding into offshore wind. The firm has shuttered its venture arm and now concentrates on real businesses with real earnings. And while the market may not yet see it, the architecture of a more focused company—perhaps even a future split—is slowly taking shape.

The path from here will not be linear. Concejo will never be fashionable. But that is precisely the point. In a market obsessed with immediacy, it offers a test of patience—and a test of principles. Should perception finally catch up to purpose, the revaluation may come not as a surprise, but as a reward long deserved.

Until then, this remains a place where capital quietly endures, waiting not for attention, but for recognition.

This is not investment advice.

Annex 1

What is their Berner Industrier share worth at 51.40 SEK?

Berner Industrier Share Price (April 2025): 51.40 SEK

Concejo's Shareholding: 1,538,123 shares

Total Value of Holding: 1,538,123 shares × 51.40 SEK/share = 88.7 MSEK

This reflects an increase from the previously reported book value of 65.1 MSEK, resulting in an unrealized gain of 23.6 MSEK. The company gained 14.4 MSEK from selling the shares at 394,200 value on SEK 36.60, excluding brokerage fees.

Original Equity (Dec 2024): 673.5 MSEK

Adjustment for Berner Holding: +23.6 MSEK

Adjustment for Berner selling price: +14.4 MSEK (394,200*36,60 SEK excl. fees)

Adjusted Equity: 673.5 MSEK + 23.6 MSEK + 14.4 MSEK = 711.5 MSEK

Total Shares Outstanding: 11,702,203

Adjusted Book Value per Share: 711.5 MSEK / 11.702 million shares ≈ 60.78 SEK

Previous Book Value per Share: 57.55 SEK

Increase due to Berner Industrier: +3.2 SEK (+5.6%)

Annex 2

Capital allocation

Concejo AB distributed the following dividends per share:

2020: SEK 17.00

2021: SEK 15.00

2024: SEK 3.00

No dividends were paid in 2022 and 2023. Total Dividends Paid per Share: SEK 35.00.

Share Price on May 26, 2020: Approximately SEK 68.80

Share Price on April 29, 2025: Approximately SEK 39.90

This represents a decline of about 42% over the period.

To calculate the Total Shareholder Return (TSR), we consider both dividends received and capital gains:

Initial Investment: SEK 68.80

Dividends Received: SEK 35.00

Ending Share Price: SEK 39.90

Total Value at End of Period: SEK 39.90 (share price) + SEK 35.00 (dividends) = SEK 74.90

Total Return: SEK 74.90 - SEK 68.80 = SEK 6.10

Percentage Return: (SEK 6.10 / SEK 68.80) × 100 ≈ 8.9%

To express this as a Compound Annual Growth Rate (CAGR) over 4.33 years ≈ 1.99%

Despite a decline in share price, the dividends received during Rosenblad's tenure resulted in a modest positive return for shareholders.

Annex 3

How to research Swedish unlisted companies?

The website www.allabolag.se provides helpful revenue and EBIT overviews for Swedish companies. The screenshot below indicates that SAL Navigation is rapidly becoming more profitable.

Annex 4

What revenue and EBIT to expect for Concejo’s most important holdings?

2021: 190 | 27.5 - Losses in Firenor and Optronics drag on EBIT

2022: 180 | 14.8 - Narrowing losses, stable growth in SBF Fonder

2023: 254 | 21.7 - Optronics profitability and Firenor turnaround

2024: 380 | 45.7 - Driven by Petrofac deals, 10% growth in SBF

2025: 460 | 58 - Ongoing contract execution and scale-up across subsidiaries

Several assumptions can be used to estimate the companies driving the value:

Estimates assume no new acquisitions or divestments affecting control.

Firenor International: Modest growth (~5%) has been consistent. With the Middle East unit fully exited and core segments stabilizing, we assume steady organic growth toward SEK 290M revenue and EBIT of SEK 18M in 2025. However, the company wrote that “over the past four years, we've achieved an annual growth rate of 50%, and we expect continued success with the recent signing of a framework.” The company refers to a message published last year when they signed a framework agreement with a minimum of NOK 500 million.

SAL Navigation: Continues stable growth (~6%). Forecast assumes SEK 155M revenue and EBIT around SEK 12M in 2025, as integration and product margins normalize.

Berner Industrier: The company keeps on performing, in line with my estimates. Concejo will not be selling more as it goes up.

SBF Fonder: Management targets 10% revenue growth and 15% EBIT margin. Applying that: 2025 revenue = SEK 69M, EBIT = SEK 10.4M, after previous years were skewed by accounting adjustments.

Optronics Technology: Strong 113% growth in 2024, driven by new framework agreements (e.g., Petrofac). Forecast assumes delivery ramps up in 2025, with SEK 130M revenue and losses narrowing as scale improves and investment slows (EBIT: -5M).

ACAF Systems: Sharp decline in 2024 (possibly due to project timing or market hesitation). Recovery is possible in 2025, assuming deals convert and demand for fluorine-free foam picks up. Conservative SEK 20M revenue and positive EBIT return.

Concejo Ventures: Concejo decided to wind down Concejo Ventures as a separate business area. All investments will be transferred to the company’s asset management, except for the investment in Envigas, which will be reported as a separate associated company. Highly volatile due to valuation swings and Envigas losses. Assuming stabilization (no major impairments), EBIT forecast at break-even in 2025.